Not everything is a data business - Anthropic announces a flurry of partnerships with data providers

New Claude plug-ins with financial data providers positions Anthropic and other leading AI platforms as a distribution layer for data companies, presenting several second order challenges and risks

Anthropic strikes again - but this time the market perceives Anthropic’s data-related product enhancements as complementary to Data & Analytics businesses, not direct challenges. More on that below.

Asymmetrix is no longer just a Substack newsletter; we are a full-fledged data and research company providing critical intelligence to stakeholders in the Data & Analytics industry. Our clients include private equity funds, investment banks / corporate finance houses, management consultants, equity analysts and more - all keen to stay up to date and informed on the Data & Analytics industry. If that sounds like you, feel free to reach out directly at sales@asymmetrixintelligence.com or via our website www.asymmetrixintelligence.com for a demo.

Maybe AI companies don’t want to be data businesses

A month after the “SaaSpocalypse” erased $300bn from publicly traded software and data companies, the Data & Analytics industry is still grappling with what rapid AI deployment means for its future.

The relationship between data businesses and AI is a sensitive one: sometimes symbiotic and synergistic and sometimes competitive. AI platforms rely on high-quality datasets either to train models or to embed data into AI workflows. At the same time, AI tools commoditize certain research tasks and public web data collection, eroding demand for data products derived from publicly available or easily scraped data.

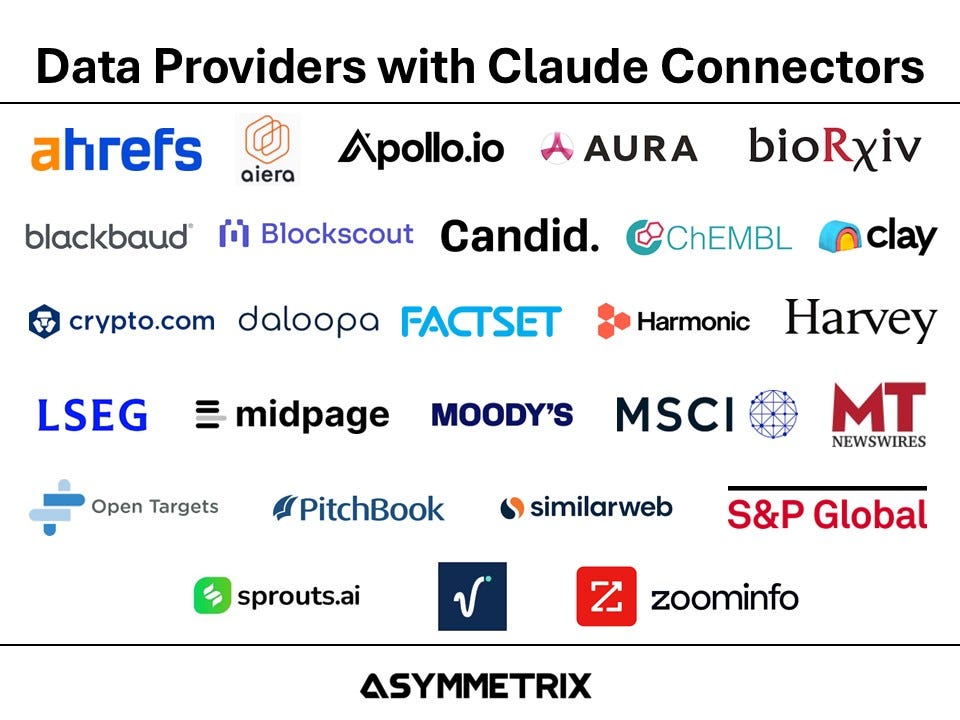

AI as distribution layer

This past week, Anthropic announced 10 new enterprise plug-ins for Claude, including several with incumbent financial data providers. LSEG, which has touted its “LSEG Everywhere” strategy, MSCI, and FactSet signed deals that will see their financial data available in Claude’s LLM workflows. Other providers announced expanded deals with Anthropic, including go-to-market platform Apollo.io. While similar announcements have surfaced in recent months, the flurry of recent announcements from Anthropic is significant because it positions LLM platforms as distribution infrastructure for proprietary datasets, not just as competitors and potential replacements.

The logic on both sides is coherent: LLM platforms recognize that replicating decades-old proprietary datasets would be difficult, time-consuming and costly. Rather than compete on data quality, LLM platforms can compete on workflow to woo enterprise clients in specific sectors.

Data providers, on the other hand, recognize that reasoning capabilities developed by LLM platforms are superior to their own and that clients likely already use LLM platforms for many adjacent or related workflows. Meeting clients where they are ensures that data providers remain relevant and are not disintermediated in favor of superior workflow solutions. Further, it widens distribution and drives new revenue for data companies, particularly in the long tail.

Clearly, AI platforms are becoming critical partners to incumbent data providers as a distribution layer – but the landscape remains fragmented. Anthropic, OpenAI, Microsoft and Perplexity have all launched enterprise AI platforms with data integrations. Data providers will likely partner broadly across platforms to ensure maximum distribution, access and usability, recognizing that some LLM platforms offer significantly better data analysis capabilities.

Brand visibility

In this new paradigm, UI will matter less as the direct customer-facing frontend interface moves away from incumbents. If AI agents become the primary interface for financial or legal professionals, incumbents risk losing mindshare and brand visibility.

However, a full shift away from incumbent frontends is unlikely in the near term. The market reaction in early February seems to have assumed AI in its fully realized state: broadly adopted across industries and integrated into workflows. That is far from the case today and may never be the case; many professionals still prefer to touch and feel their data rather than rely on intermediaries to contextualize or analyze it for them. In this paradigm, UI still matters.

Scream it from the rooftops

Regardless, when clients don’t interface directly with data providers’ frontends, a major marketing challenge emerges. This has yet to be addressed widely within the industry, but Asymmetrix believes this is a second order consequence that will demand creativity and significant resources. Data providers will have to rethink their marketing strategy and go to market with or in parallel to AI platforms, ensuring reduced visibility doesn’t translate into reduced awareness.

Data & Analytics businesses will also be compelled to market their proprietary data more explicitly. Many data providers are opaque about how they source proprietary data. As AI removes the barriers and lowers the cost of data collection, the onus is on data providers to be forthcoming and prove to the market why it is worth paying a premium for their data. In the age of AI, clients will only pay a premium for proprietary data if data providers can effectively communicate and prove that their data is differentiated – and why.

Increased competition

The advancements of AI meaningfully alter competitive dynamics in the Data & Analytics industry. The market’s initial jitters in early February not only priced in widespread adoption of AI platforms, but the possibility that datasets can be replicated quickly and cheaply. In that reading, any provider is at risk.

That reality is an unlikely one, however. Just because collecting data and building frontends for specific workflows may become relatively cheap and frictionless, that doesn’t mean that every data provider will face an AI-first competitor because someone can theoretically build it. Competition and disintermediation may not be around the corner, but the mere risk does give investors pause, inevitably driving valuations lower.

The AI reality gap

The gap between the perceived risks of AI and reality still seems to be quite wide, as the market priced in a full AI rollout and assumed AI capabilities more sophisticated than we see today, with minimal benefits accruing to the incumbent Data & Analytics providers from AI enhancement. Most AI adoption today is limited to product features, data collection tools and internal efficiencies. We have yet to see a data provider built from the ground up entirely using AI.

One of the most promising benefits of AI is in the potential for margin improvement. As we have discussed, those margin improvements have yet to materialize, at least for publicly traded companies like S&P Global. We are still in the investment phase – companies are spending heavily to roll out AI. In that vein, management at S&P and other companies have said that future internal productivity gains will offset or exceed the investment required.

Less is more

Our working view is that AI will not, in fact, lead to mass layoffs in the Data & Analytics industry, efficiency gains notwithstanding. We also believe that the Data & Analytics industry is expanding – not shrinking or consolidating around a few AI platforms. Greater efficiency will lower barriers to entry and expand the market; AI interfaces will make data more accessible and usable for a wider range of users. As data collection becomes easier, businesses will shift focus to what truly differentiates: proprietary data, curated analytics and human insight.

📜 Interesting Content

What Hath God Wrought: The Geometry of Data Markets and the Path to Data Liquidity - Freeman Lewin on X

CME rankles market data users with licensing changes - waterstechnology

AI Disruption of the Financial Services Data Industry - A Portage Perspective - Portage Partners